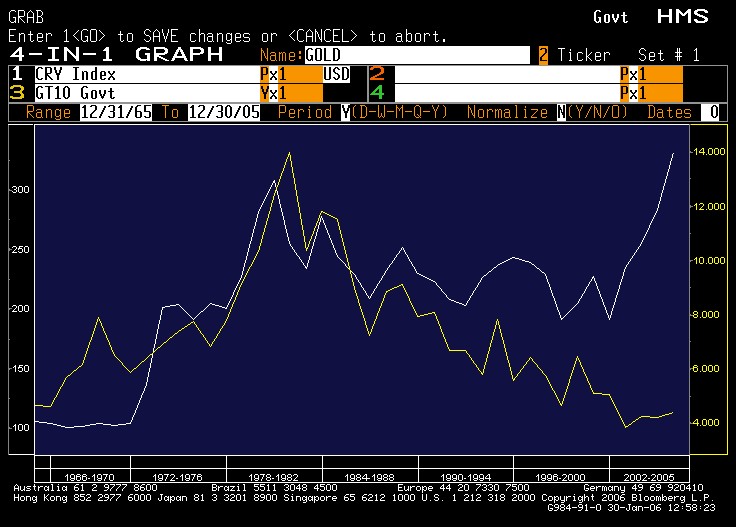

2006 opens with a huge fanfare with people chasing stocks and commodity while bonds remain subdue without signs of inflation. Is Gold forecasting future inflation or the present CPI saying that there is enough slack in the market to absorb rise in underlying commodity prices. I think that companies in the US will try to keep final goods inflation as low as possible in order to attract consumers while eating the cost in raw materials. Yes, they can do it by increasing productivity and reducing wage inflations. However, there is only so much that they can do. Sooner or later, they will have to let the price goes. The two extreme examples are: oil companies hikes prices when WTI rises, whereas walmart keeps prices stable when everything is going up. remember starbucks passes the cost of coffee increases to you too.

This is my thought of portfolio allocation:

big theme: growth in EM, revaluation of japanese stocks due to end of deflation and reforms, increase commodity use with tight supplies (oil refineries, precious metals, clean water)

Long Russia (controls european energy)

Long Asian stocks (cheap PE for the growth, but more momentum for now)

Long Japanese stocks (see above)

Short Japanese bonds (reflation)

Long Energy/ Oil (if there is growth in EM, they only like to use oil for now)

Long Precious Metals (tight supply, but big sharp runs, seems like the run of oil from 55 to 70, i think that Central banks are behind gold move)

Long Water/Agricutural (Major water problems around the world)

Long Tech (where else can large corporate achieve higher productivities, they have tons of cash)

Long Canada (seems like Chinese like to buy things from there)

Short large cap US (where can they go, they are more like bonds now)

Long Chinese stocks (seem cheap vs the rest of asian stocks and Japanese Life insurance got mandate to buy this year)

Given a lot of these have ran up in 2005 and past week in 2006, I would suggest running a 40%-60% equity/cash position. I just think that there has to be some sort of consolidation or pullback before buying. However, given the level of Chinese stocks versus the rest of Asia or EM, it might be wise to add some here.

{kind=link}