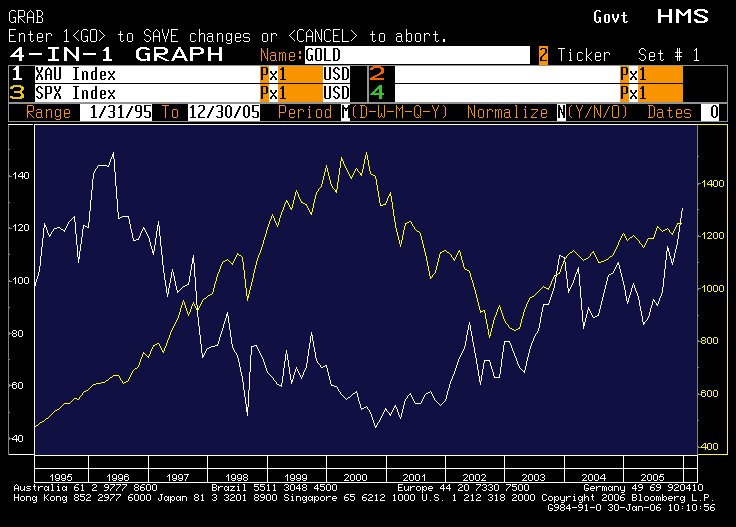

Gold Stocks vs S&P (1995-2006)

So let's think what they are going to do with their money. Central bankers will continue to buy Government bonds since they cannot take the credit risk of practically anything else. However some governments are loosening up the limits to buy real assets such as oil or mines. This will support commodity run and buffer the effect of a potential slowdown in global growth. As for the petro money, their local markets are too small for them (Middle East stock market has a huge run already). So they will look for returns in their US Dollar. They will continue to buy and to diversify from US dollar. They will buy anything with potential to generate returns higher than 10y note. Chasing equity, commodities, credit...etc Pension funds is finding it harder and harder to achieve benchmark without taking more risk.

At the fault of global central bankers, the world is full paper money. The liquidity is chasing for asset return which in terms leads to lower volatility which also keep the "asset inflation" gravy train running. Yes, there may be different assets in vogue during different times, but overall, gravy train will still be around for now.

Therefore "don't think, just follow the money".*** while it is still worth something.

{kind=link}